10 Jun 2026

Regional Tax Structures Reshape Reward Distribution Mechanisms Across Licensed Virtual Betting Sites

Regional tax structures have begun altering how licensed virtual betting sites allocate player rewards, with operators adjusting bonus systems, loyalty programs, and payout frameworks to maintain compliance while preserving margins. Data from multiple jurisdictions shows these shifts accelerating through the first half of 2026, particularly as governments refine digital gaming levies.

Tax Rate Differences Drive Structural Changes

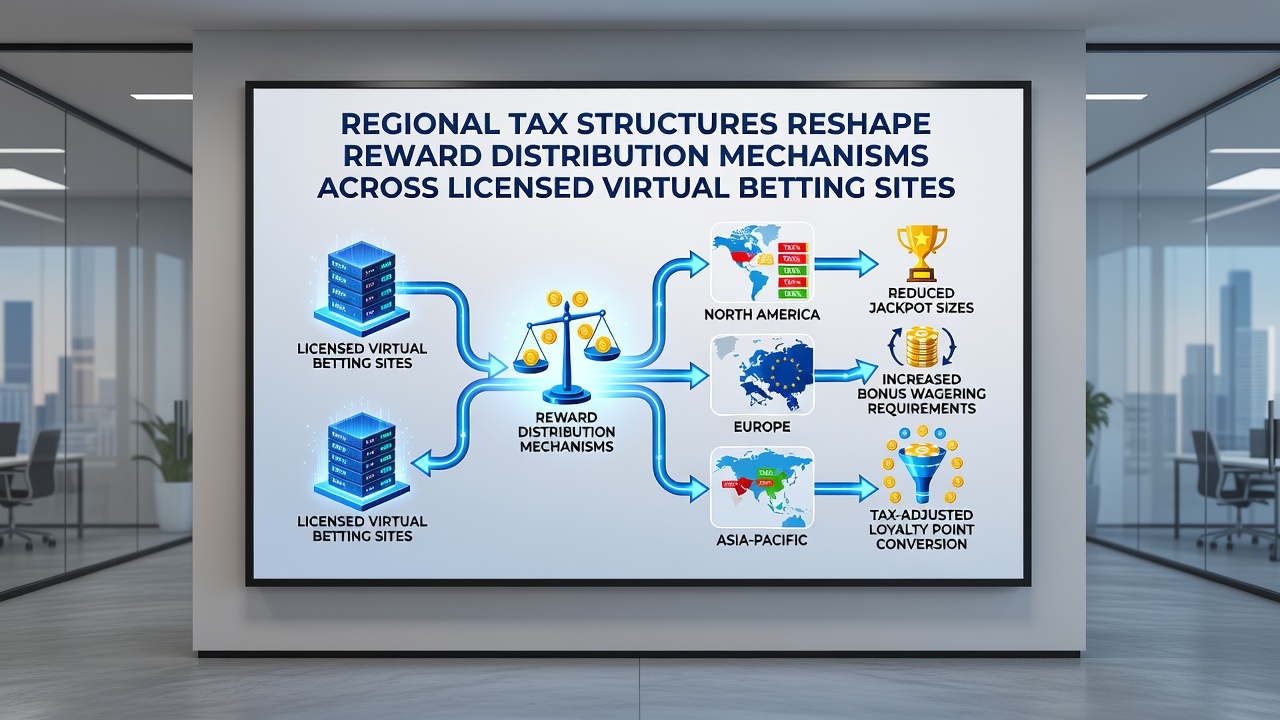

European markets demonstrate clear patterns where point-of-consumption taxes range from 15 percent in certain Eastern European jurisdictions to 25 percent or higher in Western nations, prompting operators to replace large upfront welcome bonuses with staggered reward tiers that release over extended play periods. Operators in higher-tax zones often convert cash bonuses into free spin packages or deposit-match credits that carry stricter wagering multipliers, a direct response to reduced net revenue after tax obligations.

North American frameworks present another layer of complexity, where individual state levies in places like New Jersey and Pennsylvania interact with federal considerations, leading platforms to recalibrate progressive jackpot contributions and VIP cashback percentages. According to figures released by iGaming Ontario, provincial tax adjustments implemented in early 2026 correlated with a measurable drop in standard deposit bonuses across licensed sites, replaced instead by targeted loyalty point accelerators that operators can scale based on real-time tax exposure.

Operator Adaptations in Reward Allocation

Operators respond by restructuring reward distribution through tiered loyalty systems that emphasize ongoing engagement rather than one-time sign-up incentives. Research indicates these programs frequently tie reward unlocks to deposit volume thresholds that account for tax liabilities, allowing platforms to distribute value without eroding profitability. In regions with progressive tax bands, sites have introduced segmented bonus pools that allocate higher percentages to lower-stakes players while limiting large-sum promotions that trigger elevated tax brackets.

Payment method integrations also reflect these pressures, with operators favoring e-wallets and bank transfers that minimize processing fees while supporting faster reward redemptions. This approach helps offset tax-related cost increases by reducing overhead in the distribution chain itself.

Regional Examples Highlight Varied Approaches

Australian operators operating under state-based point-of-consumption taxes have shifted focus toward tournament entry credits and leaderboard prizes, structures that spread tax burdens across multiple smaller distributions rather than concentrating value in single large bonuses. Data compiled through mid-2026 shows these formats maintaining player retention rates even as headline bonus values declined.

Canadian provincial models, particularly in Ontario, reveal similar trends where tax harmonization efforts have encouraged cross-platform reward partnerships, allowing operators to pool resources for shared promotional events. These collaborations help dilute individual tax impacts while delivering competitive player offers. Reports from the Responsible Gambling Council note that such collaborative mechanisms increased in licensed environments during the spring of 2026.

June 2026 Developments and Ongoing Adjustments

As of June 2026, several jurisdictions have introduced updated reporting requirements that further influence reward timing and structure, requiring operators to document bonus valuations separately from standard revenue streams. Licensed sites have responded by implementing dynamic reward engines that recalculate offers in real time based on current tax rates and player location data.

These engines frequently prioritize non-cash rewards such as merchandise credits, event access, or extended play time, categories that sometimes receive favorable tax treatment compared with direct monetary bonuses. Observers note this transition maintains perceived player value while aligning wth regulatory expectations across borders.

Future Implications for Licensed Platforms

Continued refinement of regional tax policies suggests reward distribution mechanisms will keep evolving, with operators investing in compliance technology that tracks jurisdictional changes automatically. Licensed virtual betting sites now treat tax structure analysis as a core operational function, integrating it directly into promotional planning cycles rather than treating it as an afterthought.

Conclusion

Regional tax variations continue to reshape how rewards reach players on licensed platforms, driving innovation in bonus design, loyalty mechanics, and cross-border operational strategies. Platforms that adapt quickly maintain competitive positioning while meeting both tax obligations and player expectations across diverse markets.